Hello and welcome to the session. This is Professor Farhad. In this session, we're going to be looking at property transactions. Specifically, we're going to be looking at a very important concept in property transactions, which is determining the gain or loss. We will also be explaining the concept of realized vs. recognized. However, if you don't know how to determine the gain or loss, realizing vs. recognizing will not be of any use to you. This topic has been covered in an income tax course, the CPA exam regulation section, as well as the enrolled agent exam. As always, I would like to remind you, my viewers, to connect with me on a professional level. If you have a LinkedIn account, please connect with me. If you don't have a LinkedIn account, I encourage you to create one. If you have a Facebook account, please like my Facebook page and connect with me on a personal level. You want to make sure you subscribe to my YouTube channel. Like the videos, share them, and put them in your favorites. Especially if you enjoy them, let your classmates know about them. Share the good news and spread the wealth. Basically, this is my Twitter feed and on my website, you can find my courses organized by course and chapter. So today, we're going to be looking at the determination of gain or loss. The first thing we want to know is how to compute or realize gain or loss. Here's the formula for it: the difference between the amount realized from the sale or disposition of the asset and its adjusted basis. Simply put, the formula is amount realized minus the adjusted basis. Let me give you a simple example. Let's assume we sold a car for $6,000. This is the amount we...

Award-winning PDF software

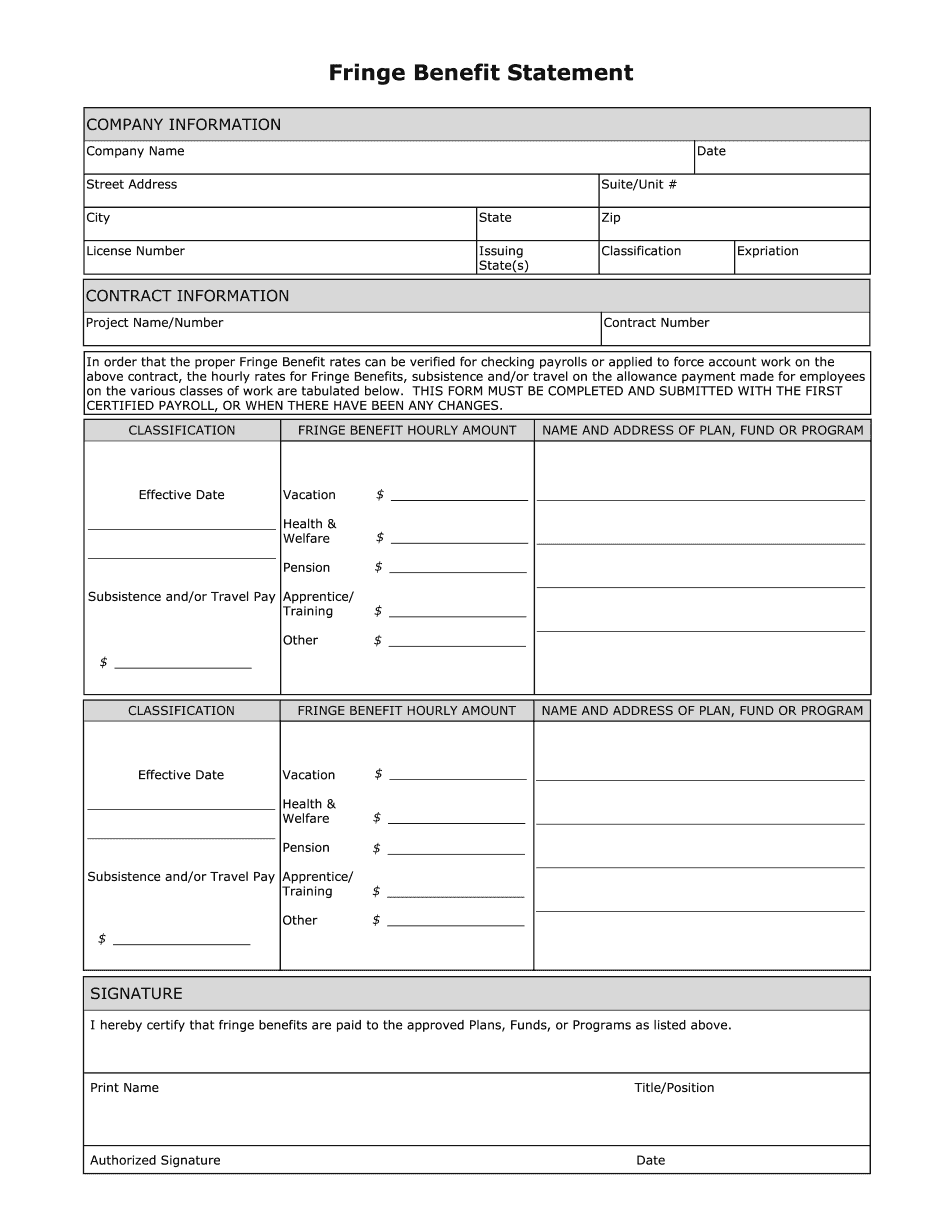

How to calculate fringe benefits for certified payroll Form: What You Should Know

The first cost of each fringe benefit to be included in the annual cost is the amount paid to each person. It can be a lump sum, or a percentage of the wages paid. It is the cost of the fringe benefits in the wages. A lump sum is when money is paid or credited directly to employee's account on payroll. In this scenario each person receives the equal monthly amount to pay their contribution. The percentage of income is the percentage of the fringe benefit to be covered. Sample Calculations For Payment Amounts The payment amounts are based on how much the actual benefit was, which would include the fringe benefits, which are the costs, time and all other associated costs to the employer. These costs are incurred by the employers and paid by the workers to the extent provided by law. Because fringe benefits were paid in lieu of any fringe benefits that normally were provided. If the benefits provided in cash, the benefit rate is 1.5% of wages for each dollar paid, and the payment can be in cash or a payroll deduction from the pay or benefits. However, the employers must pay at least 50% cash from their gross paycheck. If the benefits provided in services, the benefit rate is 1.5% of wages for each dollar paid, and the payment can be in cash or a payroll deduction from the pay or benefits. However, the employers must pay at least 55% cash from their gross paycheck. However, fringe benefits were provided in services, there is no provision for any wage contributions. For Example: Suppose you pay 5% in cash at the time of the grant of your fringe benefits contract to each recipient, for a total of 1,500. The cash would cover the fringe benefits, and the payment and services payment would both be deducted from your pay. The total reimbursement of 2,375 would be paid to each recipient out of the cash grant. If fringe benefits were provided for 5% in cash or services, the cost of each benefit is 500 × (1 + 0.25) = 500. Thus, the average payment is 450.00. However, if you did not provide the cash or services in any form, the cost of the benefits for your own service is 350 + 0.75 + 1,250 = 3,250.00. The benefit calculation is performed by an accountant. The benefit is equal to the total expense in wages, and benefits, multiplied by the total number of hours during the calendar year, plus the benefit rate.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Fringe Benefit Statement, steer clear of blunders along with furnish it in a timely manner:

How to complete any Fringe Benefit Statement online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Fringe Benefit Statement by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Fringe Benefit Statement from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing How to calculate fringe benefits for certified payroll